UMBC is committed to fostering your financial wellness by preparing you to make good, and sound financial decisions along the way. This starts with proactively managing your student financial account. Keep in mind, your financial account is in your name, therefore, the outcome of this journey is yours, not your family’s.

We get it….stuff happens. Despite your best planning, you and your family may find yourselves in a difficult financial situation. Here is some important advice and guidance, should you run into unexpected financial challenges:

- Take immediate action: If you are struggling to pay your bill, you may be inclined to simply ignore bill notices – hoping they will magically go away – but that’s not likely to happen so it’s important to read them carefully and respond. In fact, timing is critical when you’re experiencing financial difficulty as the longer you wait to address the matter, penalties could be accruing – so it’s important to address the matter as soon as possible. Manage and respond to all communications including your Financial Aid To-Do’s, and your student financial account.

- Talk with Your Financial Aid Counselor: You don’t have to navigate this process by yourself; there are individuals on campus who can help. Contact your financial aid counselor and share the circumstances you are experiencing. They are here to help and guide you. Learn who your designated financial aid counselor is here.

- Consider Low-Interest Student Loans:

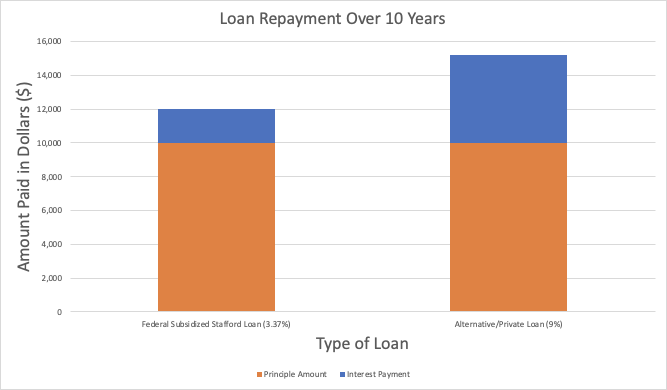

- Your education is an investment in yourself, and loans can be a great option for funding this investment . Student loans, particularly those administered through the federal government, such as the Subsidized and Unsubsidized Stafford Loans, typically have lower interest rates than regular bank loans. For example, with Fall 2021 interest rate of 3.73%, a subsidized Stafford Loan of $10,000 would require you to pay back $1,996 in interest if paid in 10 years after graduation. This means the loan costs you $11,996. However, the same loan amount at an interest rate of 9% (a range could be between 7%-13%), would require you to pay back $16,201. That’s an additional $5,201 beyond the initial amount you borrowed. If you are going to leverage loans, consider leveraging first any federal loans for which you may be eligible.

- Over 5 Years

Federal Subsidized Stafford Loan

Loan: $10,000

Interest: 3.73%

Total Payment: $11,996

Average Personal Loan

Loan: $10,000

Interest: 9%

Total Payment: $16,201

- Adjust Accordingly: If it is apparent to you that you will not be able to secure the resources needed to cover your tuition and other expenses, make adjustments as necessary but pay close attention to the posted deadlines. For example, if full-time enrollment is not financially feasible and you wish to adjust your schedule to part-time enrollment, it will be important that you do so prior to the start of classes. If you do not adjust your schedule prior to the start of classes, you will be responsible for the charges associated with full-time enrollment. For example, the difference between part and full time could be anywhere between $1,032.00 and $6,140.00 for an in-state student in the academic year 2021-2022. Similarly, if you determine you are not able to handle the expenses associated with living on campus, you will need to cancel your license with Residence Life and the Campus Card offices but you should do so by the deadlines outlined in your agreements. If you cancel after the deadline indicated in your agreement, you may be responsible for all or a portion of the charges. For example, if you cancel your housing after August 30th you could owe more than $600.

- Talk with Family and Other Supporters: Those closest to you want to see you succeed. They can be an invaluable resource in helping you strategize on how to secure the resources you need. They may even be willing to provide you some financial assistance but that requires that you talk with them first. When you do, we recommend you present them with a solid plan. Here are a few things you might want to include in your plan:

- A personal statement – Tell your story and provide insight to why pursuing your degree is important to you.

- Be truthful, don’t mislead those that want to support you!

- Your degree plan – Present your four-year, semester by semester, degree plan. Including how you plan to address the challenges that previously impacted your success. You want to inspire confidence that you have a solid plan for completion.

- Career Objective – Be clear about what you hope to do with your degree. Is your plan to do social justice work in your community? Promote art education? Pursue a career in researching medical issues affecting your family and community?

- Financial Need – It’s important that you be very transparent about your financial situation. You want your supporters to feel confident that their financial support will actually make a difference in moving you forward in pursuing your dreams and goals. If you need $1,700 to pay your balance so that you can re-enroll, then you need to be clear about that need.